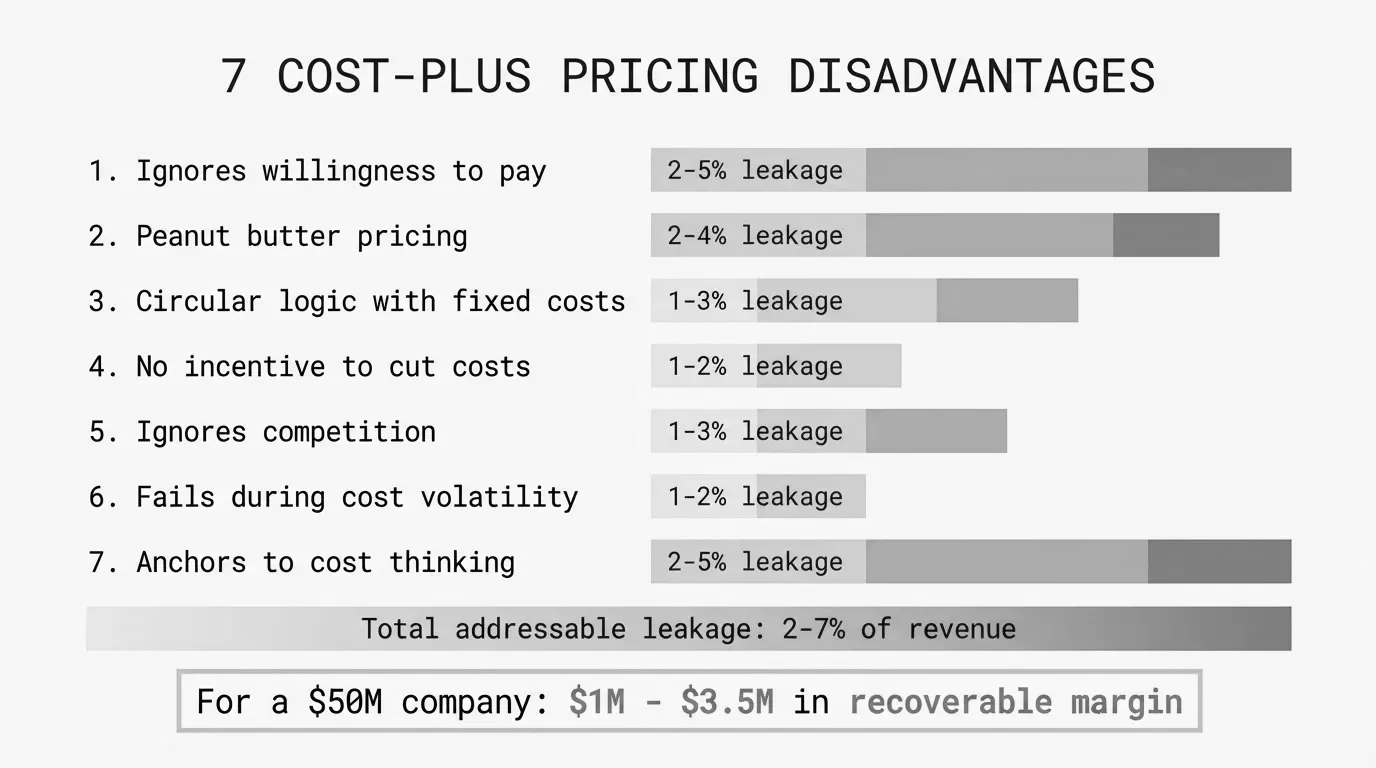

7 Cost-Plus Pricing Disadvantages That Erode Distributor and Manufacturer Margins

Cost-plus pricing is simple and defensible, but it quietly leaks margin. Here are 7 specific disadvantages and what they actually cost distributors and manufacturers.

Cost-plus pricing has a core flaw: it prices products based on what they cost you, not what they're worth to customers. This means it systematically undercharges on high-value products and overcharges on commodities where competitors have lower costs. For mid-market distributors and manufacturers managing thousands of SKUs, these disadvantages compound into millions of dollars in leaked margin every year.

That said, cost-plus isn't always wrong. It's simple, defensible, and prevents you from selling below cost. The disadvantages matter most when you're applying it as your only pricing strategy across an entire catalog of 5,000 to 100,000 SKUs with wildly different competitive dynamics and customer value.

Here are the seven disadvantages that actually cost you money, how to quantify each one, and when they're tolerable.

1. It ignores what customers will actually pay

This is the fundamental problem. Cost-plus calculates price by looking inward at your costs, not outward at customer value.

Cost-plus price = Cost x (1 + Markup %)

Value-based price = Customer's next-best alternative + switching costs + value differential

A 30% markup on a $50 commodity widget gives you a $65 selling price. The same 30% on a $200 specialty fitting that saves the customer four hours of downtime gives you $260. But if the customer's alternative costs $350 including labor, you've left $90 per unit on the table.

McKinsey's 2003 article "Pricing New Products" in The McKinsey Quarterly found that 80 to 90% of all poorly chosen prices are too low. Cost-plus is a primary driver of that pattern, because it caps your price at cost plus a margin, regardless of the value you deliver.

For a distributor with 20,000 SKUs, even 5,000 specialty items underpriced by an average of $5 each, selling 100 units per year, means $2.5M in annual margin left on the table. That's money you earned the right to capture by stocking specialized products and providing technical support. Cost-plus gives it away.

2. It treats a $2 fastener and a $200 specialty valve the same way

Cost-plus pricing eliminates price segmentation. Every product gets the same markup logic regardless of how customers buy it, how price-sensitive they are, or how easy it is to find elsewhere.

SPARXiQ CEO David Bauders calls this "peanut butter pricing" because it spreads the same markup everywhere like peanut butter on toast. The problem: your customers are price-shopping your A items (the top 20% of SKUs by revenue) and ignoring the price on your C items (the bottom 50% by revenue, which are rarely compared across suppliers).

With a flat 28% markup:

| Product type | What happens | Margin impact |

|---|---|---|

| Commodity items (A items) | Customers push back, reps discount to win | Realized margin drops to 20-22% |

| Standard products (B items) | Prices land roughly at market | Margin holds at ~28% |

| Specialty products (C items) | Nobody price-shops these | You could charge 35-42%, but you don't |

The net result is that your blended margin drifts below your target. SPARXiQ's research across hundreds of distributors' invoice data shows that pricing overrides by sales reps reduce margins by 7-10 points versus matrix values, and those overrides concentrate on the price-sensitive commodity items. Your "28% markup" becomes 20% where it matters and 28% where nobody's looking.

For more on moving beyond flat markups, see our B2B pricing strategy guide.

3. It creates circular logic with fixed costs

Cost-plus pricing requires you to know your unit cost before setting a price. But in manufacturing, unit cost depends on production volume, because fixed costs (equipment, facility, overhead) get spread across more units. And volume depends on the price you set.

This creates a loop that has no clean starting point:

- To set the price, you need unit cost

- To calculate unit cost, you need to know volume

- To forecast volume, you need to know the price

In practice, companies break this loop by assuming a volume and calculating cost from there. But if actual volume comes in lower than projected, unit costs rise, and your "profitable" price turns out to be break-even or worse.

Here's the math on a manufactured component with $500,000 in annual fixed costs:

At 10,000 units: Fixed cost per unit = $50

At 5,000 units: Fixed cost per unit = $100

Difference in unit cost: $50 (a 100% increase)

If you set a 25% markup on the 10,000-unit cost ($50 + $20 variable = $70, selling at $87.50) but only sell 5,000 units, your actual cost is $120 per unit. You're losing $32.50 on every sale. This "death spiral" effect has pushed manufacturers out of product lines entirely.

4. It removes incentive to control costs

When your price is a direct function of cost, higher costs mean higher prices, which means higher absolute profit dollars at the same markup percentage. There's no built-in pressure to reduce costs because the pricing formula absorbs them automatically.

At 25% markup:

$80 cost → $100 price → $20 profit

$90 cost → $112.50 price → $22.50 profit (cost went up, but so did profit dollars)

This looks harmless in isolation. But over time it creates organizational complacency about cost management. Why invest in process improvements or negotiate harder with suppliers when the pricing formula passes everything through?

The problem shows up when competitors operate at lower costs. Your $112.50 price on a $90 cost may be fine internally, but a competitor producing the same item for $70 can sell at $87.50 and earn the same 25% markup while undercutting you by 22%. You've priced yourself out of the market on cost-sensitive items, and your cost-plus formula provided no warning.

Government contracting has dealt with this for decades. Cost-plus contracts have been criticized for decades precisely because they reduce supplier incentive to control direct costs, indirect costs, and fixed costs. The same dynamic plays out in private-sector distribution every time a pricing matrix gets loaded with supplier costs plus a standard margin and nobody revisits it.

5. It ignores competitive dynamics

Cost-plus pricing is entirely inward-looking. It doesn't account for what competitors charge, how they're positioning, or whether your costs are higher or lower than the market.

Consider two distributors selling the same product line:

| Factor | Your company | Competitor |

|---|---|---|

| Cost from supplier | $80 | $65 (better volume deal) |

| Markup | 30% | 30% |

| Selling price | $104 | $84.50 |

| Price gap | $19.50 cheaper |

Same markup percentage. Completely different market position. The customer doesn't know or care that your costs are higher. They see a $19.50 price gap and buy from your competitor.

This is common in distribution, where supplier costs vary based on purchase volume, rebate tiers, and negotiated terms. Two distributors applying the same "30% markup" methodology can end up 15-25% apart on shelf price. Cost-plus doesn't surface this problem because it never looks outside your own cost structure.

Simon-Kucher's Global Pricing Study has consistently found that 70-80% of companies report facing a price war in their industry. Blindly following cost-plus without competitive awareness is how you end up in one.

6. It fails during rapid cost changes

During the 2021-2023 inflation spike, supplier costs in distribution moved monthly or even weekly. Cost-plus pricing in theory adjusts automatically: costs go up, prices go up. In practice, the lag kills you.

The typical pass-through cycle for a mid-market distributor using cost-plus in Excel:

- Supplier sends new price list (Day 0)

- Pricing team receives and reviews (Day 5-10)

- New costs loaded into ERP/spreadsheets (Day 10-20)

- Sales team notified of price changes (Day 15-25)

- Customer quotes reflect new prices (Day 20-30+)

During that 20-30 day window, you're selling at old prices on new costs. If your supplier raised prices 8% and you move 500 line items during the lag period, you've absorbed that entire increase on those transactions.

The reverse happens during deflation, but nobody moves as fast to lower prices. This asymmetry means cost-plus creates a ratchet effect: you eat margin on the way up and slowly recapture it on the way down. Over multiple cost cycles, the cumulative leak adds up.

For a $75M distributor experiencing four supplier price changes per year with an average 20-day lag and 5% average increase, the annual margin leak from pass-through delays alone runs roughly:

$75M revenue x (20/365 days) x 5% cost increase x 4 cycles = ~$822K in absorbed cost increases

That's before accounting for the sales team quoting from outdated price sheets, which SPARXiQ's contract pricing research found happens on 46% of transactions at some distributors.

7. It anchors your organization to cost thinking

This disadvantage is the hardest to quantify but may be the most expensive over time. When every pricing conversation starts with "what does it cost us?", you train your entire organization to think about pricing from the inside out.

Sales reps justify prices by pointing to cost. Product managers evaluate new lines based on markup potential. Finance reviews pricing by checking that margins hit the target percentage. Nobody asks: "what is this product worth to the customer?"

That organizational muscle atrophy makes it harder to transition to any form of value-based or market-based pricing later, because every process, every spreadsheet, and every conversation is built around cost as the starting point.

McKinsey's 2003 article "The Power of Pricing" in The McKinsey Quarterly by Marn, Roegner, and Zawada found that companies focused on transaction-level pricing (what each customer actually pays after all deductions) rather than cost-based list prices pushed average pocket margin up by 4% and operating profits by 60% within a year. The shift from cost-based thinking to transaction-based thinking was the catalyst, not new software.

When cost-plus disadvantages are tolerable

Not every situation demands abandoning cost-plus. The disadvantages hit hardest in specific conditions, and they're manageable in others.

Cost-plus works well enough when:

- You're selling true commodities with transparent market pricing and low differentiation

- You're passing through supplier cost increases during inflationary periods (cost-plus gives you a defensible justification)

- You're pricing a new product category where you don't yet have competitive or value data

- Your customer base is price-sophisticated and will push back regardless of your methodology

- You need audit-defensible pricing for regulatory or contractual reasons

Cost-plus disadvantages are severe when:

- You carry specialty or differentiated products (where customer value far exceeds your cost)

- You serve diverse customer segments with different price sensitivity

- Your costs are higher than competitors' for the same products

- You're managing 5,000+ SKUs where segmented pricing would capture more margin on the long tail

- Your industry is seeing frequent cost changes that create pass-through delays

For a balanced view including the upside, see our analysis of cost-plus pricing advantages and disadvantages.

What to do about it

You don't need to abandon cost-plus entirely. The most practical approach for mid-market distributors and manufacturers is to layer additional pricing logic on top of it.

Use cost-plus as your floor, not your ceiling. Calculate your cost-plus price as the minimum acceptable price. Then ask: is this product worth more to the customer? Is the market priced higher? If yes, price up.

Segment your catalog. Apply tighter, more competitive pricing on your A items (the 20% of SKUs customers price-shop). Widen margins on C items (the 50% of SKUs nobody compares). SPARXiQ's research shows this approach adds 2-4% gross margin without changing your product mix.

Measure pocket price, not list price. According to Zilliant's 2020 Global B2B Benchmark Report, B2B companies lose between 2% and 17.1% of annual margin from pricing inefficiency. Most of that leak happens between invoice price and pocket price, in the off-invoice deductions that cost-plus ignores entirely.

Start with your biggest gaps. Pull 12 months of transaction data, identify your widest margin variance by product-customer combination, and address the top 10% first. Pryse does this from a CSV upload in 24 hours.

For the complete framework, see our cost-plus pricing guide and our broader B2B pricing strategy overview.

Last updated: February 1, 2026

Frequently Asked Questions

Want to analyze your entire product catalog?

Pryse automatically identifies margin leakage across thousands of SKUs. Upload your data and find hidden profit in 24 hours.

One-time $1,499 diagnostic. No subscription required.