The Cost-Plus Pricing Formula: How to Calculate It (With Examples)

Learn the cost-plus pricing formula, markup vs margin math, overhead allocation, and worked examples for distributors and manufacturers.

The cost-plus pricing formula is the most widely used pricing method in distribution and manufacturing. It calculates selling price by adding a fixed percentage markup to the total cost of a product.

Selling Price = Total Cost x (1 + Markup %)A product that costs you $80 with a 25% markup sells for $100. Simple. That simplicity is why roughly 80% of mid-market distributors and manufacturers default to some version of this formula, according to Simon-Kucher's 2023 Global Pricing Study, which surveyed over 2,700 companies on their pricing approaches.

But "simple" and "optimal" aren't the same thing. The basic formula has several variations depending on how you calculate cost, where you allocate overhead, and whether you're targeting a markup or a margin. Confusing the last two alone can cost you 5-10 points of profit on every transaction.

Here's how to get the math right, where the formula breaks down, and what to do about it.

For the complete strategy beyond formulas, see our cost-plus pricing guide.

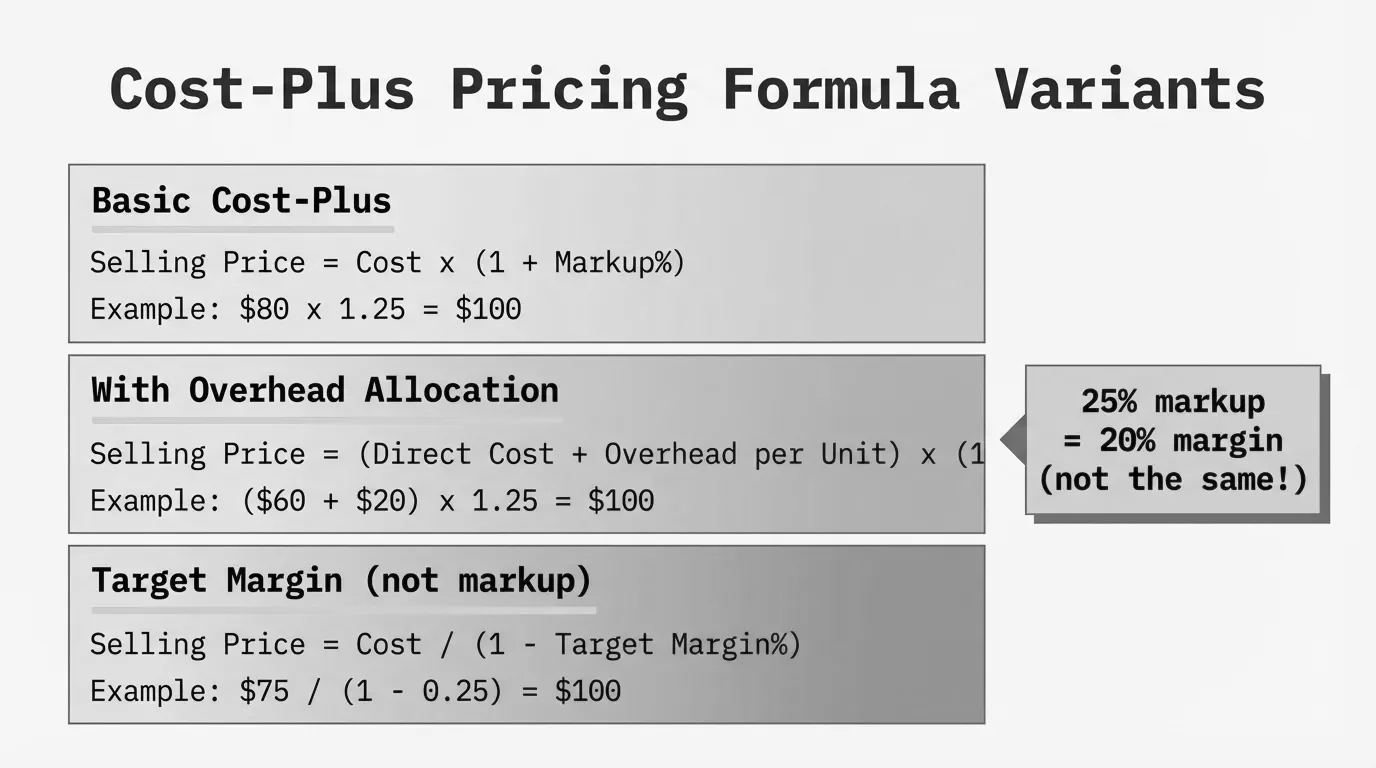

The basic cost-plus pricing formula

The foundation is straightforward. You need two inputs: your total cost per unit and your desired markup percentage.

Selling Price = Total Cost x (1 + Markup %)

Selling Price = Total Cost + (Total Cost x Markup %)

Both versions produce the same result. The first is cleaner for spreadsheets. The second makes the dollar markup visible.

Example: Electrical distributor

You buy a box of industrial connectors from the manufacturer for $42 per box. Your target markup is 30%.

Selling Price = $42.00 x (1 + 0.30)

Selling Price = $42.00 x 1.30

Selling Price = $54.60

Your profit per box is $12.60. Your markup is 30%. Your margin is 23.1%. (More on that distinction in a moment.)

Example: Contract manufacturer

You produce a custom bracket. Direct materials cost $6.20. Direct labor is $3.80. Your target markup is 45%.

Direct Cost = $6.20 + $3.80 = $10.00

Selling Price = $10.00 x (1 + 0.45)

Selling Price = $14.50

This is the bare-bones version. It works when your direct costs are clear and overhead is already covered by volume. But for most manufacturers, overhead is a significant chunk of the real cost, and ignoring it in the formula means your markup isn't actually covering what you think it is.

Cost-plus pricing with overhead allocation

The basic formula uses direct costs only. The full-cost version adds allocated overhead, which gives you a more accurate picture of what each product actually costs to deliver.

Fully Loaded Cost = Direct Costs + Allocated Overhead per Unit

Selling Price = Fully Loaded Cost x (1 + Markup %)

Overhead includes everything that isn't directly tied to a single unit: rent, utilities, equipment depreciation, warehouse labor, insurance, IT systems. You allocate it to products using a rate based on direct labor hours, machine hours, or another driver that reflects how products consume those resources.

Overhead Rate = Total Overhead Costs / Total Allocation Base

Allocated Overhead per Unit = Overhead Rate x Units of Allocation Base per Product

Example: Manufacturer with overhead allocation

Your plant runs $1.2M in annual overhead. You expect 60,000 direct labor hours this year.

Overhead Rate = $1,200,000 / 60,000 hours = $20.00 per direct labor hour

Product A takes 0.5 direct labor hours to produce. Direct materials cost $15. Direct labor is $12.

Allocated Overhead = $20.00 x 0.5 hours = $10.00

Fully Loaded Cost = $15.00 + $12.00 + $10.00 = $37.00

Selling Price (at 35% markup) = $37.00 x 1.35 = $49.95

Without overhead allocation, you'd price off $27 in direct costs, and your 35% markup would give you $36.45. That's $13.50 below the fully-loaded price. At 500 units a month, that's $6,750 in monthly margin you'd never see.

The choice of allocation base matters. Labor-intensive operations typically use direct labor hours. Automated lines use machine hours. The key is picking a base that reflects how overhead is actually consumed. A product that ties up a CNC machine for 2 hours should absorb more overhead than one that runs for 10 minutes, even if the labor time is identical.

Cost-plus with target margin vs. target markup

Here's where companies get into trouble. Markup and margin are not the same number, and using the wrong one in your formula changes your selling price.

Target markup formula (markup on cost):

Selling Price = Cost x (1 + Markup %)Target margin formula (margin on selling price):

Selling Price = Cost / (1 - Margin %)These produce different results. If your CFO says "I want 30% on that product," you need to know whether they mean 30% markup or 30% margin. On a $100 cost item:

30% markup: $100 x 1.30 = $130.00

30% margin: $100 / (1 - 0.30) = $100 / 0.70 = $142.86

That's a $12.86 difference per unit. On 10,000 units, it's $128,600 in annual profit you either capture or don't, depending on which formula you use.

The margin-based formula is what you want when your P&L targets are expressed as gross margin percentages, which is how most finance teams think. The markup formula is simpler and more common on the operations side, where people think in terms of "how much do we add to cost."

Markup vs. margin: the conversion table

This confusion costs real money. SPARXiQ's analysis of distributor pricing data shows that sales reps commonly round markups to numbers ending in 5s and 0s (25%, 30%, 35%), and many don't realize the margin those markups actually produce.

Here's the conversion table every pricing manager should have pinned to their wall:

| Markup % | Margin % | Multiplier |

|---|---|---|

| 10% | 9.1% | 1.10 |

| 15% | 13.0% | 1.15 |

| 20% | 16.7% | 1.20 |

| 25% | 20.0% | 1.25 |

| 30% | 23.1% | 1.30 |

| 35% | 25.9% | 1.35 |

| 40% | 28.6% | 1.40 |

| 45% | 31.0% | 1.45 |

| 50% | 33.3% | 1.50 |

| 75% | 42.9% | 1.75 |

| 100% | 50.0% | 2.00 |

The conversion formulas:

Margin = Markup / (1 + Markup)

Markup = Margin / (1 - Margin)

A distributor targeting "25% margins" who uses 25% markup in their pricing matrix is actually getting 20% margins. Across a $50M book of business, that 5-point gap is $2.5M in gross profit they think they're earning but aren't.

For a quick conversion tool, see our markup to margin calculator. For a deeper dive into margin math, check the gross margin formula breakdown.

Worked example: Distribution scenario

Let's walk through a complete cost-plus pricing calculation for a mid-market electrical distributor with 15,000 SKUs.

Setup:

- Product: 100-amp circuit breaker

- Manufacturer cost (landed): $68.50

- Inbound freight allocation: $2.15 per unit

- Warehouse handling cost: $1.80 per unit

- Target markup: 28%

Total Cost = $68.50 + $2.15 + $1.80 = $72.45

Selling Price = $72.45 x (1 + 0.28)

Selling Price = $72.45 x 1.28

Selling Price = $92.74

Margin check:

Gross Profit = $92.74 - $72.45 = $20.29

Gross Margin = $20.29 / $92.74 = 21.9%

That 28% markup translates to a 21.9% gross margin. If your finance team targets 25% gross margin, you need to adjust. Using the margin-based formula:

Selling Price = $72.45 / (1 - 0.25)

Selling Price = $72.45 / 0.75

Selling Price = $96.60

The difference is $3.86 per unit. For a product you move 200 units per month, that's $9,264 in annual margin from getting the formula right.

The reality check: This circuit breaker is a commodity product that customers price-shop. Competitors might sell it at $89-$91. Your cost-plus formula says $92.74 or $96.60, but the market says $90. This is exactly where cost-plus hits its limits: it tells you what you need to charge, not what you can charge. More on that below.

Worked example: Manufacturing scenario

Now a custom-fabrication manufacturer running $85M in revenue with 8,000 active SKUs.

Setup:

- Product: Stainless steel mounting plate (custom spec)

- Raw material: $22.40 per unit

- Direct labor: 1.2 hours at $28/hour = $33.60

- Overhead rate: $45 per direct labor hour (includes equipment, facility, quality)

- Target gross margin: 32%

Direct Costs = $22.40 + $33.60 = $56.00

Allocated Overhead = $45.00 x 1.2 hours = $54.00

Fully Loaded Cost = $56.00 + $54.00 = $110.00

Using the target margin formula:

Selling Price = $110.00 / (1 - 0.32)

Selling Price = $110.00 / 0.68

Selling Price = $161.76

Cross-check with markup:

Markup = $161.76 - $110.00 = $51.76

Markup % = $51.76 / $110.00 = 47.1%

A 32% margin requires a 47.1% markup on fully loaded cost. If this manufacturer had used "32% markup" instead of "32% margin," they'd have priced at $145.20 and actually earned a 24.2% margin. On a run of 1,000 units, that mistake costs $16,560.

Now here's where it gets interesting: this is a custom-spec part. The customer can't buy it from three other suppliers. The next-best alternative is a different alloy or a different design that requires rework on their end. In this scenario, cost-plus gives you a floor, but value-based pricing could justify $175-$185. The formula is useful but incomplete.

Where the cost-plus formula breaks down

The formula works as a starting point. It falls apart as a complete pricing strategy, especially at scale.

Problem 1: It treats all products the same. A flat 28% markup across 15,000 SKUs means you're earning the same percentage on a $2 commodity fitting (where the customer will switch suppliers over a nickel) and a $200 specialty valve (where they'd pay $260 without blinking). SPARXiQ's research on distributor pricing found that reps using flat cost-plus approaches sacrifice 1-2 full margin points compared to segmented pricing, and that this practice commonly affects 30% or more of revenue.

Problem 2: It ignores the customer's alternative. Your cost doesn't determine what the product is worth to the buyer. A $110 custom mounting plate that saves the customer $400 in assembly time is underpriced at $161. Cost-plus can't see that.

Problem 3: It's slow to adapt. When your supplier raises prices, the formula automatically raises your selling price. But it doesn't account for competitive response. If your competitors absorbed part of the increase, you've just priced yourself out. And it definitely doesn't help when raw material costs drop but you're still pricing off last quarter's landed cost.

Problem 4: It doesn't account for cost-to-serve. Two customers buying the same product at the same markup look identical in the formula. But one orders 50 units on a scheduled PO with net-30 terms. The other orders 3 units at a time, demands same-day delivery, calls your inside sales team twice per order, and pays at net-60. Your real margin on the second customer is 8-12 points lower, and cost-plus can't see it.

Problem 5: Accuracy depends on overhead allocation. If your overhead rate is based on normal capacity but you're running at 60% utilization, your products are absorbing less overhead than they should. Your "fully loaded" cost is understated, and your margins are thinner than you think. The reverse is true at high utilization: you over-allocate and potentially overprice.

According to Zilliant's 2020 Global B2B Benchmark Report, which analyzed over 1 billion B2B transactions, pricing inconsistencies and routine pricing issues cause 1.9% to 13.4% margin leakage. Cost-plus contributes to this because it creates a false sense of precision. The formula is exact, but the inputs and assumptions behind it are full of gaps.

When cost-plus pricing still makes sense

Despite its limitations, cost-plus is the right starting point in several situations:

New product launches where you don't have competitive or customer data yet. Price to cost-plus, then adjust as you learn what the market will bear.

Commodity products where differentiation is minimal and the market sets the price. Cost-plus tells you whether you can play in that market profitably. If your cost-plus price is above market, you either reduce cost or exit the product.

Cost pass-through agreements where your contracts with customers specify that price changes follow input cost changes. Many distribution agreements work this way for core products.

Price floor guardrails in any pricing strategy. Whatever method you use to set the actual selling price, cost-plus gives you the minimum. Sell below that floor and you lose money on the transaction. McKinsey's 2003 article "The Power of Pricing" in The McKinsey Quarterly by Marn, Roegner, and Zawada showed that a 1% price decrease erodes operating profits by 8% for the average S&P 1500 company. Pricing below cost-plus accelerates that damage.

The practical approach for most mid-market companies: Use cost-plus as the floor, competitive data as the reference, and customer willingness-to-pay as the ceiling. The formula gives you a starting number. Market reality tells you whether to adjust up or down.

Getting your costs right

The formula is only as good as its inputs. "Garbage in, garbage out" applies directly to cost-plus pricing. Here's where cost calculations commonly go wrong in distribution and manufacturing:

Landed cost isn't purchase price. Your actual cost includes inbound freight, duties, handling, and receiving labor. A $50 item with $4 in landed cost additions has a true cost of $54. Marking up $50 by 30% gives you $65. Marking up $54 by 30% gives you $70.20. That $5.20 difference per unit adds up fast across thousands of SKUs.

Costs change faster than price lists. If your ERP updates product costs monthly but your supplier changes prices quarterly (or more often during inflationary cycles), your markup is applied to stale data. SPARXiQ's research shows that distributors lagging more than 30 days on cost pass-through lose 1-2 margin points on the affected products.

Rebates and incentives complicate the picture. If you earn a 2% rebate from your supplier on annual volume, your effective cost is 2% lower than what's in your ERP. Some companies factor this into their cost-plus calculation. Others treat it as found margin. The right answer depends on how predictable the rebate is and whether you've already committed the volume.

For most mid-market companies running cost-plus in Excel or a basic ERP, the biggest quick win isn't a fancier formula. It's getting the cost inputs accurate and current. A correct cost-plus price beats a sophisticated formula applied to wrong numbers every time.

Next steps

If you're running cost-plus pricing in spreadsheets across thousands of SKUs, you already know the pain: stale costs, inconsistent markups across reps, and no visibility into what your realized margins actually look like after discounts and off-invoice deductions.

Start by checking the gap between your intended markup and your actual margin. Pull a sample of 100 transactions and calculate the realized margin on each one. If the spread between your highest and lowest margin is more than 15 points, your cost-plus formula isn't the problem. Execution is.

For a deeper look at how cost-plus fits within a broader pricing approach, see our cost-plus pricing guide. For worked examples across different industries, check out our cost-plus pricing examples.

Last updated: February 1, 2026

Frequently Asked Questions

Want to analyze your entire product catalog?

Pryse automatically identifies margin leakage across thousands of SKUs. Upload your data and find hidden profit in 24 hours.

One-time $1,499 diagnostic. No subscription required.