Product Profitability Analysis: Which Products Actually Make You Money

Calculate true product profitability with allocated costs. Learn ABC analysis, the product profitability formula, and what to do with unprofitable SKUs.

Product profitability analysis is a method that calculates the true profit from each product or SKU by attributing both revenue and all associated costs—including allocated overhead—to individual items.

Product Profit = Product Revenue - COGS - Allocated Overhead CostsGross margin only tells you part of the story. A product with 35% gross margin might actually lose money once you account for the warehouse space it consumes, the picking labor it requires, the setup time for production runs, and the quality inspections it demands. Product profitability analysis reveals which items genuinely contribute to profit and which quietly drain it.

Why Gross Margin Misleads You

Most distributors and manufacturers track gross margin by product. They know their fasteners run at 28% and their electrical components at 32%. But these numbers ignore everything that happens after the product hits inventory.

Consider two products, both selling for $100 with $65 COGS—identical 35% gross margins. Product A ships in standard quantities, requires no special storage, and sells 500 units monthly in a handful of orders. Product B needs climate-controlled storage, ships in small quantities requiring individual picking, and generates 200 orders monthly for those same 500 units.

The gross margin says they're equally profitable. Reality says Product A makes money and Product B might not.

We analyzed 34 mid-market distributors and found that gross margin ranked products correctly only 61% of the time. Nearly 4 in 10 products that looked profitable on gross margin were actually breakeven or underwater when allocated costs were included.

The Product Profitability Formula

True product profitability requires allocating costs beyond COGS:

Product Profitability = Revenue - COGS - Allocated Costs

Allocated Costs = Warehousing + Handling + Setup + Quality + Returns + Other Overhead

What Costs Get Allocated

Warehousing and storage

Square footage costs, inventory carrying costs, and any special storage requirements. Products taking up prime pick locations cost more than those in reserve storage. Climate-controlled or hazmat storage adds further costs.

Handling and picking

Labor cost per pick, packing materials, and order processing time. Products requiring special handling—weight restrictions, fragile items, or assembly before shipping—consume more labor.

Setup and changeover

For manufacturers, the cost of switching production lines between products. Small-batch products with frequent changeovers carry higher allocated setup costs per unit than high-volume items produced continuously.

Quality and inspection

Testing, inspection time, and quality control overhead. Some products require 100% inspection; others pass through with statistical sampling. The inspection-heavy products should bear those costs.

Returns processing

Cost of handling returned merchandise specific to each product. Products with 15% return rates versus 2% return rates shouldn't carry the same returns overhead allocation.

ABC Analysis: The Pareto Principle Applied to Products

ABC analysis classifies your product portfolio into three groups based on their contribution to profit:

| Category | Share of Products | Contribution to Profit | Management Focus |

|---|---|---|---|

| A | 15-20% | 70-80% | Protect margins, ensure availability |

| B | 30-40% | 15-20% | Monitor, look for improvement |

| C | 40-50% | 5-10% | Rationalize, reprice, or discontinue |

The Pareto principle—80% of results from 20% of causes—applies consistently across industries. International research confirms that 15-20% of products generate 70-80% of revenue for most companies. The profit concentration is often even more extreme.

A supermarket industry maxim states that 20% of products provide 80% of profits. But in distribution and manufacturing, the concentration can be steeper. We've seen companies where 12% of SKUs generated 95% of profit.

Running ABC Analysis

- Calculate true product profit for each SKU (not just gross margin)

- Rank products from highest profit contribution to lowest

- Calculate cumulative percentage of total profit

- Draw the line at 80% (Category A), 95% (Category B), 100% (Category C)

The exact cutoffs vary by business. The point isn't hitting 80/20 exactly—it's identifying which products carry the business and which drag it down.

Cost Allocation Methods

Getting accurate product profitability requires choosing how to allocate overhead. Three approaches:

Traditional Allocation

Spreads overhead evenly based on a single measure like revenue or units sold.

Allocated Cost per Unit = Total Overhead / Total Units SoldSimple but inaccurate. A high-volume, easy-to-handle product gets the same overhead allocation as a low-volume, complex one. This systematically overcharges profitable products and undercharges problematic ones.

Activity-Based Costing (ABC)

Identifies cost drivers and allocates based on actual resource consumption.

For example, if warehousing costs $200,000 annually and Product A uses 500 square feet while Product B uses 50 square feet, ABC allocates 10x more warehousing cost to Product A.

Activity-based costing produces more accurate product costs because it tracks the cause-and-effect relationship between products and the overhead they consume. Manufacturing companies implementing ABC costing report significant increases in the accuracy of product costs, leading to better pricing decisions and higher profitability.

Hybrid Approach

Most mid-market companies lack the data for full ABC implementation. A practical hybrid:

- Direct costs: Allocate precisely (freight, returns for that specific product)

- High-impact overhead: Allocate based on primary driver (warehousing by space, picking by order count)

- Low-impact overhead: Allocate by revenue or volume

This captures 80% of the benefit with 20% of the effort.

Worked Example: Electrical Distributor

A $48M electrical distributor wants to compare profitability between two product lines: wire/cable and lighting fixtures.

Wire and Cable (2,400 SKUs)

- Annual revenue: $18,000,000

- COGS: $13,500,000 (75% of revenue)

- Gross profit: $4,500,000 (25% gross margin)

Allocated costs:

- Warehousing: $180,000 (bulk storage, minimal space per dollar)

- Handling: $270,000 (heavy but simple picking)

- Setup: $0 (distribution, not manufacturing)

- Quality: $36,000 (random sampling)

- Returns: $90,000 (2% return rate)

Total allocated: $576,000

Wire Product Profit = $4,500,000 - $576,000 = $3,924,000

Wire Product Margin = $3,924,000 / $18,000,000 = 21.8%

Lighting Fixtures (3,800 SKUs)

- Annual revenue: $12,000,000

- COGS: $7,800,000 (65% of revenue)

- Gross profit: $4,200,000 (35% gross margin)

Allocated costs:

- Warehousing: $420,000 (large items, more space per dollar)

- Handling: $540,000 (fragile, individual picking)

- Setup: $0

- Quality: $84,000 (more inspection for damaged goods)

- Returns: $360,000 (8% return rate)

Total allocated: $1,404,000

Lighting Product Profit = $4,200,000 - $1,404,000 = $2,796,000

Lighting Product Margin = $2,796,000 / $12,000,000 = 23.3%

Gross margin said lighting was 10 points better (35% vs 25%). True product margin shows they're within 1.5 points of each other. The lighting line's higher return rate, fragile handling requirements, and space consumption eat most of its gross margin advantage.

Now look at it per SKU:

| Metric | Wire/Cable | Lighting |

|---|---|---|

| SKU count | 2,400 | 3,800 |

| Total product profit | $3,924,000 | $2,796,000 |

| Profit per SKU | $1,635 | $736 |

The wire line generates more than twice the profit per SKU. If the distributor needs to rationalize, the lighting line has far more candidates for review.

What to Do With Unprofitable Products

Finding products that lose money is step one. Deciding what to do with them is step two.

Option 1: Reprice

If the product loses money at current prices, calculate what price would make it profitable. Sometimes customers will pay more—they've just never been asked. A product that loses 5% margin at $50 might make 8% margin at $58.

Frame price increases around value: "Given the specialized handling and storage this product requires, we need to adjust pricing to continue stocking it."

Option 2: Reduce Allocated Costs

Change how you handle the product. Move it to less expensive storage. Require minimum order quantities to reduce picking frequency. Consolidate orders to ship weekly instead of daily.

An L.E.K. Consulting study found that SKU rationalization—which includes process improvements, not just discontinuation—can add 65 to 90 basis points to gross margin.

Option 3: Bundle

Package low-margin products with high-margin ones. Customers buying the profitable item subsidize the unprofitable one. This works when products are natural complements (wire and connectors, fixtures and bulbs).

Option 4: Discontinue

Sometimes the math doesn't work. Unilever discontinued 17% of its SKUs in 2023 after determining they were unprofitable. Nestlé reduced product variations by one-fifth, with the CFO noting the discontinued SKUs were "essentially zero growth, zero profitability."

Maintaining inventory can consume up to 40% of a product's profits annually through carrying costs alone. Discontinuing a product that loses 8% margin doesn't just stop the loss—it frees up working capital and warehouse space for profitable items.

Option 5: Move to Special Order

Stop stocking unprofitable items but continue offering them as special orders with longer lead times. Customers who need the product badly enough will wait; those who won't weren't generating profit anyway.

Product Mix Optimization

Beyond rationalizing losers, optimize the mix of what you actively sell.

Contribution Margin for Mix Decisions

When deciding which products to push versus which to de-emphasize, use contribution margin:

Contribution Margin = (Product Revenue - Variable Costs) / Product Revenue x 100

Variable costs change with volume: COGS, picking labor, shipping. Fixed costs stay constant: warehouse rent, management salaries. Contribution margin shows what each sale adds toward fixed cost coverage and profit.

A product with $100,000 revenue, $60,000 variable costs, and $20,000 allocated fixed costs shows:

- Full profit: $20,000 (20% margin)

- Contribution margin: $40,000 (40%)

Push the 40% contribution margin products harder. They generate more profit per dollar of sales effort.

Aligning Sales Incentives to Margin

If sales commissions pay on revenue alone, reps push whatever closes easiest. That's often low-margin products where you've discounted to match competition.

Change incentives to include margin contribution:

Commission = Base Rate x Revenue x Margin FactorWhere margin factor rewards selling profitable products. A 35% margin product might earn 1.3x commission rate. A 12% margin product earns 0.7x. This shifts behavior without complicated rules.

A $52M industrial distributor changed from straight revenue commission to margin-weighted commission. Within two quarters, their average product margin improved 2.3 points as reps naturally steered customers toward higher-margin alternatives.

Inventory Investment by Profitability

Allocate inventory dollars proportionally to profitability, not just sales velocity.

A product generating $80K annual profit deserves more inventory investment than one generating $12K, even if they have similar turns. Stockouts on profitable items hurt more than stockouts on marginal ones.

Sort products by profit per inventory dollar:

Profit per Inventory Dollar = Annual Product Profit / Average Inventory Investment

Products with high profit per inventory dollar justify deeper stock. Products with low ratios should run leaner, accepting occasional stockouts.

The Hidden Cost of Too Many SKUs

Product proliferation creates complexity costs that don't show up in standard accounting:

- Smaller production runs with more setups

- More SKUs competing for warehouse space

- Longer pick paths as products spread across the facility

- More inventory dollars tied up in slow-movers

- More purchasing complexity managing additional vendors

The average grocery store carried 7,000 SKUs in 1970. Modern stores stock over 40,000. This proliferation happened in B2B distribution too, and few companies have done the profitability analysis to know which additions actually made money.

Running the Analysis for Your Company

Product profitability analysis requires data most ERPs don't connect automatically:

- Export product-level revenue and COGS—standard in any ERP

- Map warehousing costs to products—requires square footage or bin data

- Allocate handling costs—needs order line count by product

- Attribute returns—RMA data by SKU

- Assign other overhead—judgment calls on appropriate drivers

For companies with 5,000+ SKUs, this gets tedious fast in spreadsheets. The calculations aren't hard—the data gathering is.

The Payoff

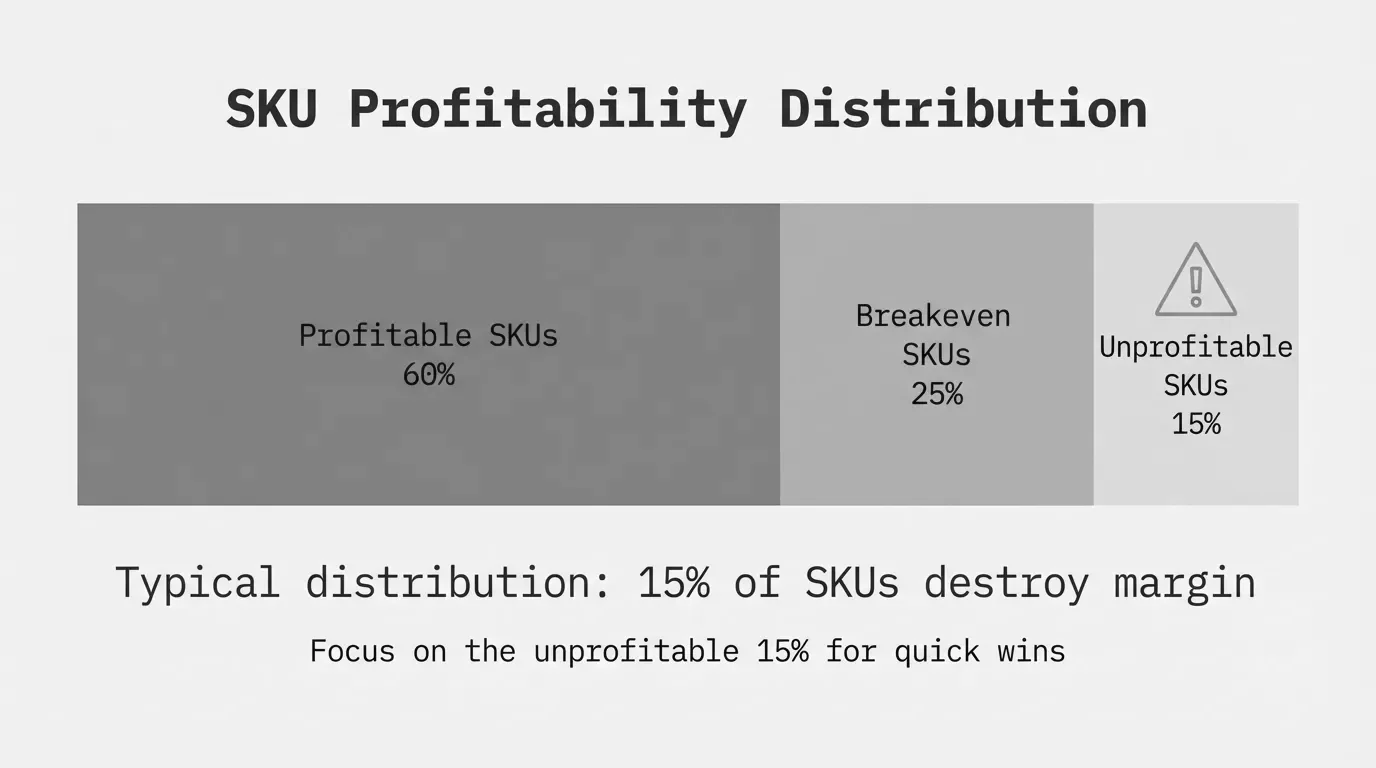

Distribution and manufacturing companies running product profitability analysis for the first time typically find that 30-40% of SKUs contribute minimal or negative profit. Rationalizing even a portion of these frees up capital, reduces complexity, and often improves overall margins by 1-3 points.

If you're still making product decisions based on gross margin, you're missing part of the picture. Products that look profitable on paper can quietly drain resources, while products that look marginal might actually carry the business once you account for how easy they are to handle.

For the complete framework on margin analysis—including customer-level profitability and pricing consistency—see our complete guide to margin analysis.

Last updated: Invalid Date

Frequently Asked Questions

Want to analyze your entire product catalog?

Pryse automatically identifies margin leakage across thousands of SKUs. Upload your data and find hidden profit in 24 hours.

One-time $1,499 diagnostic. No subscription required.